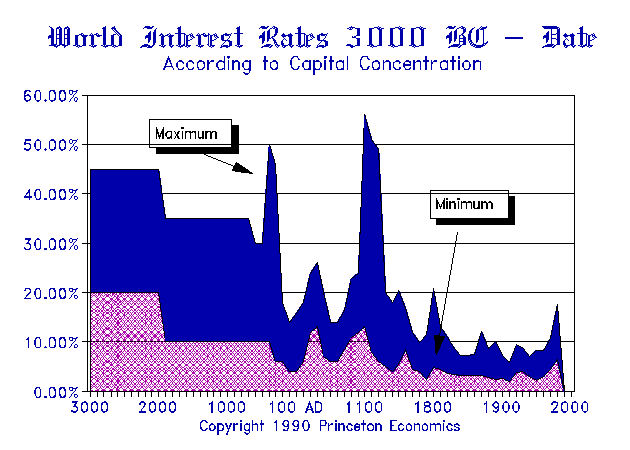

The Fed & the Future

While everyone seems to be placing a huge question on whether the Fed will raise rates or not, the markets have already factored in the rate rise for some time. The Fed was scheduled to raise rates in June, but the IMF turned to the press to criticize them to prevent a rate hike. Then in September, the IMF, ECB, and other governments all pleaded with the Fed not to raise rates. The trend will change. The Fed has no choice and that seems to be what the pundits do not get. We can see that rates are BELOW the historic low of the Great Depression, but they are also at a 5,000-year low in interest rates on a global scale as well.

The Fed is not faced with a bubble, so others like Larry Summers tell the Fed that they should not raise rates. Yet, Summers admitted that they cannot forecast the business cycle because it is far too complex. At the same time, Summers admits that the Fed typically needs to lower the rates in a recession by 3% and they have no such room from here. This is the conventional view. They can never see anything coming anyway so they just try to forecast whatever trend is in motion should stay in motion.

The crisis is more than hedge funds going belly-up in fixed income. The same is unfolding in pension funds. Keeping rates low to try to “stimulate” borrowing lowers the value of money to zero and wipes out savings for something that has never worked. Then we have taxation and enforcement rising, which even Keynes said was wrong during a recession. This is all about the greed of politicians and nothing else. There is no giant conspiracy controlling the world. No one in their right mind would run it this way. We are flying in a plane where the pilot died at the wheel and nobody knows because the cockpit door is locked. None of the theories they use to control society have ever worked, which is why the “crowd” has NEVER been able to forecast a single economic change in trend.

Looking ahead, there is absolutely no question that rates will go nuts. It appears that the Fed pressure will rise sharply in March. Do not forget that as capital flows into the USA, we will see asset inflation (stock market rise) and the gap between the non-investing and those who invest (the “rich”) will widen. This will increase the pressure on the Fed to raise rates to stop the bubble, which will be caused from external sources and not some socialistic agenda.

We will be putting together a special report on the Yield Curve, which will create tremendous problems for central banks, hedge funds, and be the real harbinger of chaos. This report is not currently available, but we will make an announcement once it is ready. So for now, sit back and enjoy the show. The longer the Fed appeases the rest of the world, the worse the future will become. Money has a value and it is not ZERO.

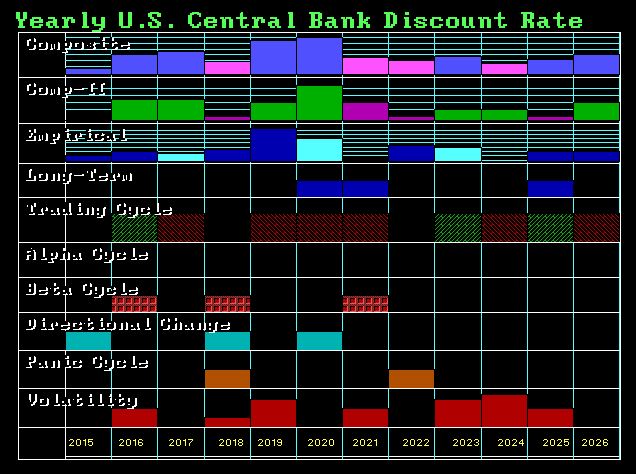

PS: Inside Socrates, we have the Fed discount rate, VIX, and Fed funds.

Financial Instability & the Fed

The argument that the Fed should do nothing because it will be harder to correct a rate rise than to do nothing because there is no bubble anywhere, demonstrates that we have the most serious BUBBLE in history. Retail participation in markets is still off by 50% from 2007 highs. People have invested in fixed income and now there is a crisis in fixed income hedge funds. The bubble is in low interest rates (GOVERNMENT) rather than the markets. This is what our computer has been projecting for 2015.75. It is right before everyone’s eyes, yet they cannot articulate what they cannot see.

The crisis was created by the ZERO interest rates. This has wiped out the elderly and destroyed the so-called American Dream. The middle class has been collapsing since government taxes them under the pretense that Social Security is a savings for their future when in fact it is just a tax. If that money had been invested in equities when the Dow was 1,000, there would be no crisis today. Pension have chased long-term rates, driving them lower and lower in an attempt to meet their future obligations.

China poured more concrete in three years than the USA did in nearly a century. This has driven the commodity markets and that has come to an end. China thus is blamed for the slow down and for the decline in its currency, which they call a war and manipulation. The trend has simply changed.

Combining these elements does not speak well of the future. The Fed is between a rock and a hard place. It will be blamed no matter it does. Nobody seems to understand the dynamics of the trend in motion.

Why Europe Will Collapse: Schultz’s Outrage at Poland

A huge protest against the Europe Union has taken place in Poland. When I was there, everyone I spoke to was against joining the euro. They all said that the euro would destroy Poland as it did in Greece and the rest of Southern Europe. European Parliament President Martin Schulz (SPD) has said that the protests in Poland have a “coup-character” because they are realistic and against the policies of Brussels, whom refuses to review or admit that the euro has been a complete disaster for Europe as a whole.

Poland has responded with indignation, making it clear that the people have a democratic right and have acted within the rule of law. Prime Minister Beata Szydlo demanded on Monday for an apology from Schulz for his statement. But Luxemburg’s Foreign Minister Jean Asselborn warned on behalf of the EU presidency that independence of the judiciary and the media in Poland is threatened. Indeed, the threat to any democratic right comes from Brussels.

Schulz said on German radio that “right-wing populists” are the greatest threat when they argue against his policies and take government into their own hands to accuse external forces to interfere in the internal politics of their country. These comments from Schultz are dictatorial in nature, as they say that anyone who disagrees with the federalization of Europe going into the hands of Brussels is a threat. A threat to what — freedom? There is no hope of trying to reason in Brussels. This is beyond hope. We must crash and burn until the end for they will NEVER admit the slightest error in their ideas.

Austria — It Started the Collapse in Great Depression. Will It Do so Again?

In 1931, the sovereign debt crisis and banking system collapse began in Austria with the failure of Credit Anstalt, which was partly owned by the Rothschilds. The bank was forced to absorb another bank and a secret loan was created in London off the books to hide the insolvency to do the merger for political purposes. When that failed to be enough, the whole scam was exposed and a CONTAGION spread as people wondered what government had manipulated behind the curtain.

Now the International Monetary Fund (IMF) has come out and stated that Austria’s banks need to increase their capital buffers urgently. The capital buffers in Austria are thin and cannot withstand a crisis. Furthermore, the banks are still active in politically and economically risky countries, which is typically carried out to increase profits. In reality, the IMF led to the loans granted by the banks in Swiss francs, which caused many borrowers to lose 30% when the peg broke. In some Eastern European countries, the potential losses by a state arranged forced conversion of Swiss franc into local currencies could be massive. This is being done because the borrowers now owe 30% more than what they borrowed due to currency risk. This situation will not magically evaporate for they are private loans.

The Austrian banks are typically banks engaged in RELATIONSHIP banking rather than TRANSACTIONAL. Therefore, they rely on customer deposits short-term and lend long-term. These are not big investment banks as in New York. They have lost a fortune because of the Swiss/euro peg collapse.

The three major banks are Erste Group, Raiffeisen Bank International (RBI), and UniCredit subsidiary Bank Austria. These are the biggest lenders in Eastern Europe as a whole who have gotten caught up in the currency nightmare. The RBI has recently announced their withdrawal from certain markets following a serious currency related loss that the bank has written in the past year for the first time. Bank Austria checked the sale of its branch business.

This coming banking crisis is all currency related. It is, of course, thanks to Brussels and their irresponsible design of the euro. Politics and economics do not go together. They will blame the bankers, but they will never blame government. Hence, this is why we can no longer afford career politicians for they will NEVER accept responsibility for screwing up the economy for political gain.

The Clintons are responsible for removing ALL restriction from the Great Depression upon the banks. They then eliminated the right to declare bankruptcy on student loans. Yet, the press will NEVER ask Hillary anything about that or the fact that her biggest contributors are the banks in NYC.

Market Talk – December 15th, 2015

All Asian markets failed to show positive signs but it was the Nikkei that was probably more of a concern, having rejected the 19k figure despite a strong open and morning session it eventually closed -1.65%.

Core Europe saw a strong day with all Indices going from strength to strength. We saw UK inflation data which helped FTSE along but had a negative impact on Gilts. the talk of the morning was how oil turned itself around aiding all core equity markets but at the expense of core Bund and peripherals bond markets. The more oil rallied the more equity markets rose. All this ahead of the FED tomorrow.

As we saw some good numbers (US CPI 0.2% M/M and Core CPI +2% Y/Y) which matched the Fed’s target for the first time since 2014. This incentivised both the US equity markets and the US Dollar. The DOW finished with an impressive +0.9% gain (+156pts) off its days high of 17,625 but an impressive performance all the same in front of the highly anticipated Fed hike. Oil gained around 3% on the day with TWI and Brent both up around $2 each at 36.77 and $38 respectively.

Given the strong CPI data the Bond market took a bit of a heat today. With US 10’s losing around 7bp has put the yield at the close around 2.26%. In Germany the 10yr Bund also lost ground closing this evening at 0.65% (puts the spread at +161bp).

In currencies the USD powered ahead with the DXY (US Dollar Index) closing with gains of +0.6% at 98.23. Core currencies (JPY, GBP and EUR) lost around 0.7% each.

No comments:

Post a Comment