CalPERS – Buying the High in Bonds? Oh Boy.

CalPERS, California Pension Plan for government workers, is adopting policies that demonstrate that they are incapable of managing money. They cannot handle the “volatility” in stocks so they are moving into bonds, and whatever shortfall they produce should be made up with higher taxes. If you are in California, my condolences. This is a strategy that will cause more government pension funds across the country to follow their lead. You just can’t make up this stuff. Selling stocks and buying what amounts to a 5000 year low in rates (high in bond prices). And you wonder how steep the cliff might be on the other side of the ECM? No, we do not advise CalPERS. I imagine government entities will not use our service until they have no choice.

Velocity of Money & the Boom and Bust Cycle

QUESTION:

Mr. Armstrong;

Is the velocity of money an indicator of booms and bust? Didn’t the QE program by the Fed increase the money supply? Then why do we not see an increase in velocity or inflation?

Confused & Curious

TW

TW

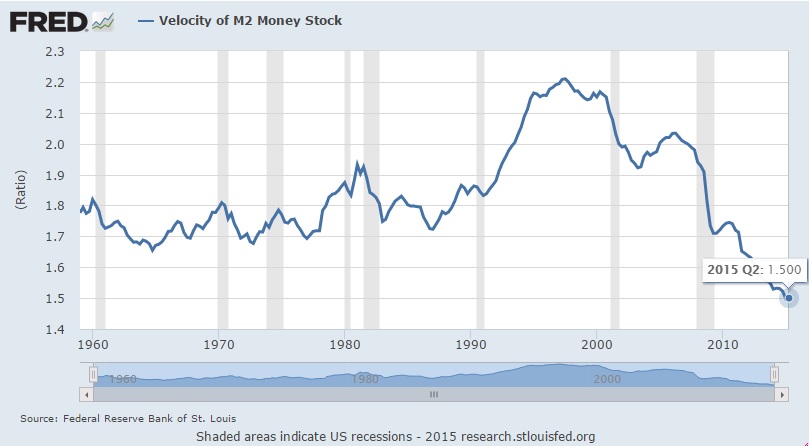

ANSWER: The reality is, in a broad general sense, the velocity of money is a reflection of the boom and bust cycle. However, the proper understanding of this indicator is greatly distorted by international capital flows. This plain vanilla explanation as applied to a closed domestic economy with some merit insofar as people spend freely during a boom and hoard their cash during a recession. Therefore, we can see from the chart that indeed we are in an age of deflation making historical lows as we enter the turning point on the Economic Confidence Model – 2015.75. However, things get a bit distorted when you assume that inflation nor velocity rose as the money supply increased because of QE1-3. That was the selling cry of the gold promoters that QE1-3 will create hyperinflation so buy gold. The exact opposite took place, showing that they are clueless about economics and are indeed just trying to sell something.

First: Debt is money, so the Fed buying in 30 year bonds and replacing them with cash in a true sense did not increase the “real” money supply since you can post bonds as collateral as they are used by central banks and commercial banks as reserves. Once upon a time, there was a distinction, as you could not borrow against government bonds before 1971. However, that vanished when debt became money. You trade futures and keep your money in T-bills, so debt has replaced cash. There is no distinction anymore. This was merely like take a $100 bill and swapping it for five $20 bills.

Second: If debt and money are one-in-the-same from a true money supply perspective, then the Federal Reserve DID NOT increase the money supply, they increased liquidity — that is a huge difference. Hence, inflation has not raised its head and velocity continues to fall because people are indeed hoarding money more so than assets. This is why retail participation in equities remains at historic lows and things like gold have declined rather than rallied. It is a question of liquidity vs. money supply.

Third: We do not live inside a fish bowl where the domestic economy is within the control of the Federal Reserve, no less some sinister dark conspiracy group. The economy is porous and as such, China said thank you to QE1-3 and sold their 30-year bonds, swapping their long-term paper for short-term. So again, the Fed’s attempt to inject liquidity by swapping bonds for cash totally failed for there was no guarantee that the bonds they were buying back were from Americans. The liquidity injection moved offshore.

Fourth: The Federal Reserve is not in control of the economy by any means unlike the Bank of Japan. Why? In Japan, you cannot issue debt in Japanese yen without approval of the Japanese government. When it comes to dollars, anyone can issue debt in dollars. Post-2007, emerging market countries have issued nearly $9 trillion worth of debt denominated in dollars to save on interest expenditures. They sucked up dollar liquidity, so again there was a total absence of inflation while the economy recovered, but marginally more like a dead cat bounce.

I understand this can be very confusing. That is caused by the fact that they still teach antiquated economic theories in school that are a barbarous relic from the past in and of themselves, and nobody with real world experience is willing to step back into academia to reshape theory. The only people who have to deal at this level tend to be international hedge fund managers who must watch the entire world. So the press airs domestic opinions and Fed the watches while there is a lot more going on behind the curtain.

The Federal Reserve is trapped. They MUST raise rates to “normalize” the economy. With rates at virtually zero, there is less of an incentive to invest or to keep your money in a bank. We have reasonable bank balances that are probably the most I have ever kept in my entire life in a non-interest yielding checking account. The bank keeps offering 0.5% for fixed CDs and my response is that I would rather hand it to a homeless person. I remain nimble, short-term waiting for the turn. So just because cash deposits at no interest may be at highs keeping VELOCITY low, it does not mean that will not change with the turn of the blink of an eye. Then you will see gold rise, but not before.

No comments:

Post a Comment