Socrates Invitation Launch

The expanded Beta Testing is now launching first to a group of 300 clients. We expect to have the full launch to the general public by early September. This stage does not have the inquiry function yet. We are finishing that code currently. You will be able to have Socrates read its analysis to you even while you drive, but being able to speak to it over the internet will be part of a later launch of Phase II.

We will post shortly some of the text output on selected markets so you can catch a glimpse at its global analysis.

Hillary Will Not Reform Banks

Hours after Hillary Clinton vowed to crack down on Wall Street, yet will by no means will she reverse what she and her husband did inrepealing Glass-Steagall. Hillary’s adviser comes from none other than Goldman Sachs, who some call the modern day Rothschilds. If Hillary is elected, she will be perhaps far more corrupt than just about anyone in the field.

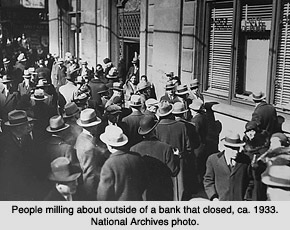

Why The Federal Reserve Worked during the 1930s

When the Great Depression began, over 8,000 commercial banks belonged to the Federal Reserve System, but nearly 16,000 did not. There were still state banks which were not members. Those nonmember banks operated in an environment similar to that which existed before the Federal Reserve was first established back in 1914. People criticize the Federal Reserve all the time, yet offer no viable alternative.

The two-tier banking environment harbored the causes of banking crises itself in addition to the Sovereign Debt Crisis. One primary cause was the banking collapse was the practice of counting checks in the process of collection as part of banks’ cash reserves. You could write a friend a check for $1 billion and he writes you a check for $1 billion and under this system you are both billionaires while waiting for checks to clear. These “floating checks” were therefore counted in the reserves of two banks, the one in which the check was deposited and the one on which the check was drawn. In reality, however, the cash resided in only one bank assuming it did not bounce in the end.

Bankers at the time referred to their reserves using these floating checks constituting fictitious reserves. The quantity of fictitious reserves rose throughout the 1920s as the economic boom unfolded and it peaked just before the financial crisis in 1930 during the last quarter of 1929. This meant that the banking system as a whole had much lower actual cash (or real) reserves available in emergencies than appeared on the surface thanks to counting these floating checks as reserves.

Additionally, without membership in the Federal Reserve, nonmember banks were plagued by their inability to mobilize bank reserves in times of a crisis. Nonmember banks kept a portion of their reserves as cash in their vaults and the bulk of their reserves as deposits in correspondent banks in designated cities. Most of these correspondent banks belonged to the Federal Reserve System. However, this interestingly created a reserve pyramid whereby these state or local country banks had no access to reserves during times of crisis. Whenever a nonmember bank needed cash because of a run by its customers, the bank had to turn to its correspondent, which might be faced with requests from many banks simultaneously. The correspondent bank also might not have the funds on hand because its reserves consisted of floating checks in the mail, rather than cash in its vault. If such a shortage unfolded, then the correspondent bank would turn and request reserves from yet another correspondent bank. That bank, in turn, might also have a shortage of cash reserves available.

FDR signs Glass–Steagall Act

Glass-Steagall was enacted because one bank created a major panic. These problems of floating checks being attributed as reserves turned the collapse of Caldwell and Company into a major financial event. Being located in Nashville, many people assumed the Southern banks were safe since they were out of New York. However, the Nashville bond trading house Caldwell & Co. was in very serious trouble because of the bond market. Caldwell & Co was Nashville’s largest bank. When the market crashed in late 1929, the ripple effect set into motion a series of events that would eventually bankrupt Caldwell’s teetering empire. Some of the industrial companies owned by Caldwell & Co. lost huge amounts of money or went bankrupt. The bond issues that Caldwell had bought as a trading company, could not be sold to the public since there was just no bid.

Caldwell has been a rapidly expanding conglomerate and the largest financial holding company in the South. It provided its clients with an array of services – banking, brokerage, insurance – through an expanding chain controlled by its parent corporation headquartered in Nashville, Tennessee. This served as the model why Glass-Steagall was enacted. The parent company got into trouble when it invested too heavily in securities/bond markets and lost substantial sums when stock prices declined. In order to cover their own losses, the leaders drained cash from the corporations that they controlled.

The problem of the floating checks being counted as reserves warns that the reserves of European banks using the bonds of all members introduces a similar potential risk. As members get into trouble post 2015.75, we can see a cascade event in the banking system. Just as Caldwell went down and took the South with it, the interconnections between banks and correspondent banks still remains to this day. While checks are no longer counted as reserves until they clear, the need for one central bank and one quality of reserves was documented during the Great Depression. The bulk of the more than 9,000 bank failures took place among nonmember banks.

The problem of the floating checks being counted as reserves warns that the reserves of European banks using the bonds of all members introduces a similar potential risk. As members get into trouble post 2015.75, we can see a cascade event in the banking system. Just as Caldwell went down and took the South with it, the interconnections between banks and correspondent banks still remains to this day. While checks are no longer counted as reserves until they clear, the need for one central bank and one quality of reserves was documented during the Great Depression. The bulk of the more than 9,000 bank failures took place among nonmember banks.The Truth About the 1933 U.S. Banking Holiday

Herbert Hoover’s memoirs (1951) documents the fact that Franklin D. Roosevelt (FDR) played a very dirty game of politics. There were rumors that FDR would confiscate gold. These rumors spread and people ran to banks to withdraw their funds. The night before the election in 1932, FDR denied that he would do such a thing. After FDR won the election, the real bank panic began. FDR would not take office until March 1933.

The run on banks began as the Great Depression started. In 1929 alone, 659 banks closed their doors due to mismanagement and speculation. However, as the 1931 Sovereign Debt Crisis hit, the number of bank failures skyrocketed. By 1932, an additional 5,102 banks went out of business. Families lost their life savings overnight. Thirty-eight states had adopted restrictions on withdrawals in an effort to forestall the panic. Bank failures increased in 1933, and Franklin Roosevelt deemed remedying these failing financial institutions his first priority after being inaugurated.

Hoover pleaded with FDR to please come out and address the gold confiscation rumors. At 1:00 a.m. on Monday, March 6, 1933 President Roosevelt issued Proclamation 2039 ordering the suspension of all banking transactions, effective immediately. He had taken the oath of office only thirty-six hours earlier.

The terms of the presidential proclamation specified:

[N]o such banking institution or branch shall pay out, export, earmark, or permit the withdrawal or transfer in any manner or by any device whatsoever, of any gold or silver coin or bullion or currency or take any other action which might facilitate the hoarding thereof; nor shall any such banking institution or branch pay out deposits, make loans or discounts, deal in foreign exchange, transfer credits from the United States to any place abroad, or transact any other banking business whatsoever.

For an entire week, Americans would not have access to banks or banking services. They could not withdraw or transfer their money, nor could they make deposits.

The crisis had been a long time coming. In the three years leading up to it, thousands of banks had failed. But a new round of problems that began in early 1933 placed a severe strain on New York banks, many of which held balances for banks in other parts of the country. About 4,000 banks failed during this period alone bringing the total to over 9,000.

Yanis Varoufakis Behind the Curtain

Yanis Varoufakis and his battle behind the curtain. Here is the full transcript of an interview with him where he speaks frankly about the battle to save Greece.

IMF Says Greek Debt Should be Foregiven

Even the IMF has come out now and warned that Greece may need a complete debt write-off. That is sending an economic earthquake through Europe for it undermines the political position of Merkel entirely. There is no doubt about this, Greece cannot pay and cannot raise taxes yet simultaneously still have any viable economy. This is the collapse of Socialism.

So why has the IMF turned around? If Greek’s debt is not written off, the harsh economic conditions being imposed will merely send Greece into the waiting arms of Russia. This is now becoming political with the IMF agreeing with the Obama position.

Market Talk

The markets were relatively well behaved today with little geopolitical excitement to unnerve trading but we did see weaker economic data in the States. Retail Sales was expected +0.2% but failed to deliver showing at -0.3%, ex-autos -0.1% verses 0.5%. Also, May Business Inventories broadly in-line at 0.3%.

Despite the less optimistic showing the US Stocks put in a reasonable performance gaining between 0.45 and 0.66% DJI and NASDAQ.

We did see an impressive performance from the US Treasury market (guess to be expected with such a weak Retail Sales) and that managed to tighten some of the spread differential lost over the Bund yesterday. Today that spread (TY/RX) tightened 5bp to trade late at 144bp.

The benchmark Greek indicator, we show daily is the GGB (Greek Government Bond), was a little weaker and marked at 25.5% in late trade. Traders normally detest quiet days but after the torrent of storms we have had to endure recently – today was a breath of fresh air.

Don’t expect it to last!

No comments:

Post a Comment