Yanis Reveals EU Denial of any Right of the People to Vote

Greece’s Finance Minister Yanis Varoufakis has come out and revealed the quite shocking and anti-Democratic events that took place during the last Eurogroup meeting. First, they do hate Yanis’ guts for he does understand far more about the economy than anyone in Brussels. Any further discussions they demand will be without him. What led to the EU breaking off was exactly what we reported previously – they do not want any member state to EVER allow the people to vote on the Euro. Brussels has become a DICTATORSHIP and is so arrogant without any just cause that they know better than the people.

We are watching the total collapse of Democracy and the birth of a new era – Economic Totalitarianism from Arrogant people who are totally clueless beyond their own greed for power and money.

The Greek Tragedy Continues to Set the Tone = World In Review

The Greek drama, ot Greek Tragedy, continues with a rumored agreement to continue the stimulus in return for promised reforms only to have Greek Prime Minister Alexis Tsipras announce a surprise referendum on July 5: after June 30 which puts the IMF payment into default. Late last week EurAsia Group’s Ian Bremmer remained confident that the Greek Parliament will approve the agreement at the last minute. Meanwhile Greek politicians demonstrate their commitment to election promises of anti-austerity while the Troika talks tough on reforms to appease their own electorate. Monday is the Eurozone Summit while Tuesday the Greek IMF payment will go into default. Next week promises to be a volatile week in the markets with the arrays showing a turning point in many markets on Wednesday.

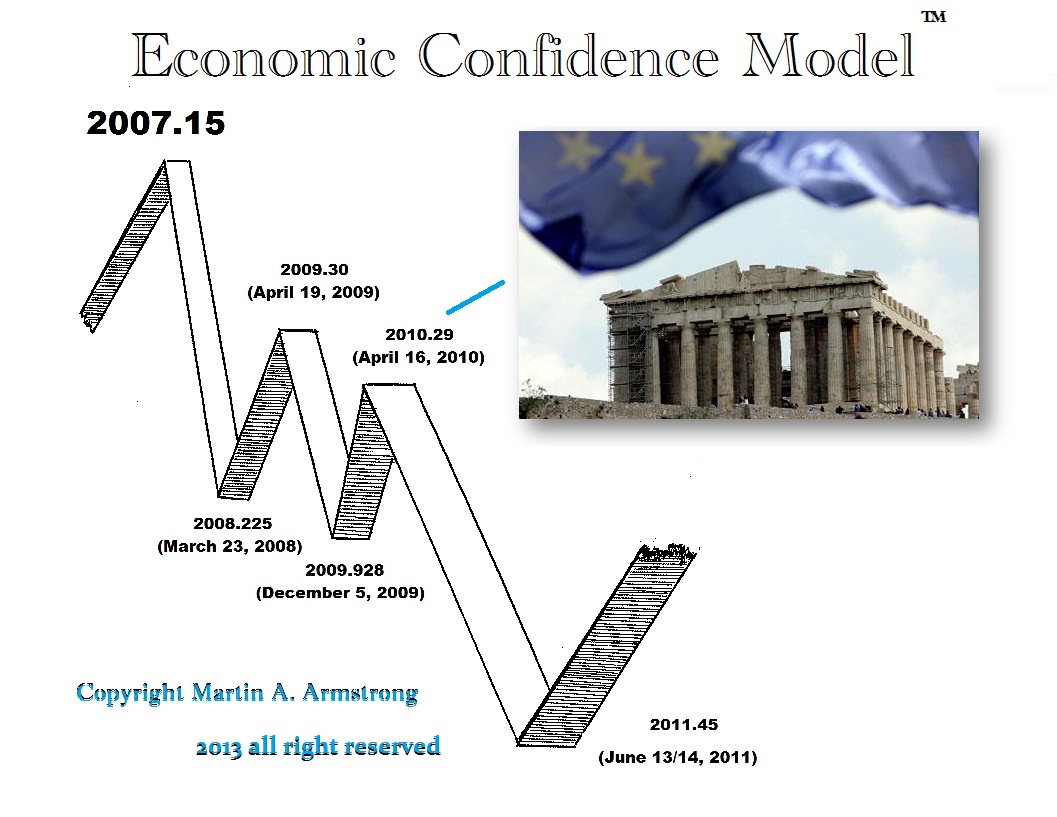

Summer volatility has continued as the market gyrates with subsequent news reports on Greek negotiations. The entire Greek debt tragedy began precisely on the Pi target to the day of our Economic Confidence Model. Everything remains stunningly on track.

Global stock markets (MSCI WD) were flat on the week ending June 26 up 13 bps as strength in Europe (MXEU up 2.78%) offset declines in North America which fell 41 bps. European markets were led by the DAX which ended the week up 4.1% holding onto gains early in the week. Despite recent strength the MXEU is down 4.8% from highs in mid-April led by the DAX down 8.3% from its peak. Meanwhile German Bund futures continued to fall 1.2% on the week bringing QTD losses on Bund futures to 5.4%. In a sign of geographic divergence, the S&P finished the week down 40 bps. Meanwhile strength in the Japanese stock market (NKY up 2.64%) offset weakness in Hong Kong and Australia as the MXAP finished the week relatively flat at +43 bps.

Precious metals gold and silver rallied to resistance in mid-June as peripheral bond yields rose. They have since turned back down as European political risk subsides with the expected Greek agreement. Industrial metals continued their sell-off demonstrating global economic weakness. Palladium prices are down 12.6% MTD while copper prices are down over 10% since mid-May despite the recent bounce.

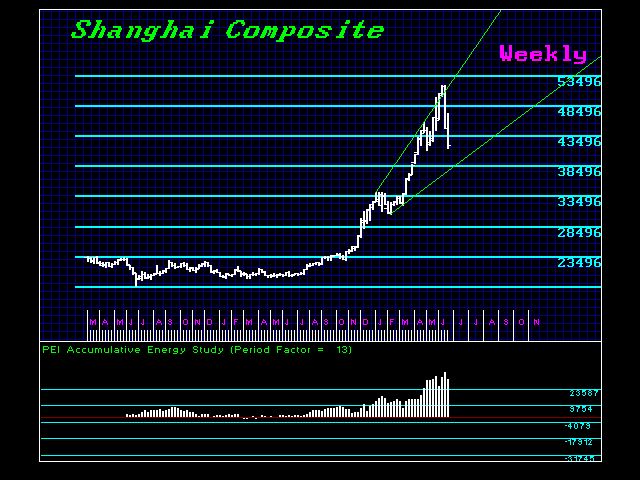

While Greek negotiations captured the attention of the media, the big shift in trend is the sell-off of Chinese stock indices with the Shanghai composite down 7.4% on Friday bringing losses to 19% since the peak on June 12. While we elected the Daily Bearish Reversals from the high, we have not yet elected a Weekly Bearish. The rally to the high was right on target 17.2 weeks from the February low (2 * 8.6).

The Chinese A share market has been historic, rising 150% in less than a year versus the 1928-29 US market rally of 100% which occurred over 18 months. This rally has been fueled by margin trading, with margin debt up 464.57% over the past year — from $R400 million last June 19 to $R2.2 billion on June 19 of this year. In an apparent response to the stock correction, China lowered benchmark interest rates and reduced bank reserve requirements on Saturday.

While the Chinese market has been the global outperformer over the past year, long term performance has lagged, with the Shanghai index failing to break the high of 6,124 set on October 16, 2007. The recent rally halted after hitting the Monthly Bullish Reversal at the 4695820.closing May at 4611744. Penetrating the low of May technically will bring the market back through the Breakout Channel. Indeed, the market has not exceeded the Breakout Line from the 2008 low.

Bond Markets Flash Caution

Much like the Chinese share market, developed world economies have been sustained by debt. While the press emphasizes high equity valuations, the debt market is the bubble. According to the Institute for International Finance, developed economy debt/GDP is at 245% excluding financial debt. While the financial sector has reduced leverage materially, the public sector debt-to-GDP ratio has increased 50 percent points in aggregate since 2000.

While emerging markets have stronger balance sheets, the rapid rise in debt is concerning, as total debt to GDP has risen precipitously from roughly 50% in 2000 to 80% at the end of 2014 as shown in the chart to the right. China has been a major driver, as debt has risen 72 percentage points versus GDP excluding financial companies.

Today the bond market displays the warning signs of rising volatility with low volumes on rallies. The German Bund has broken through its upward channel from the beginning of the 2014 and testing the 2008 trend line. Liquidity in the bond markets is dismal as brokerage houses continue to reduce inventories, reminiscent of the 2008 bond market collapse. This time, the lack of liquidity has spread to sovereign bonds including the German bund and US treasuries. The Central Banks assume they can control the sovereign bond markets, yet rates continue to rise despite OECD rate cuts and continued bond purchases in Germany and Japan.

So what will cause the bond market to correct in the absence of growth? Fixed income investors have enjoyed a 34 year (4 * 8.6) rally with rates falling since 1981 (1980 for the US). The bond markets like all markets are based upon confidence. When bond investors start losing money and realize that governments may not be able to repay their debts, they will lose confidence. Tax increases only cause economic contraction as seen in Japan and Europe. Low sovereign yields fail to protect investors from falling prices causing corporate bonds to outperform. US HY has a total return of 3.3% YTD meanwhile the Barclays 20+ treasury total return index is down 6.9%.

Central Bankers in Norway, Russia, South Korea and New Zealand have all cut rates in the past month. Yet developed market interest rates continue to rise. Eventually central bankers will be forced to raise rates to attract capital as the emerging markets are doing now. Brazil and several African countries (Namibia, Uganda and Kenya) raised rates in June to stabilize FX markets. The Brazilian real is down 15% YTD and almost 30% over the past year. While central bankers speak of inflation, the inflation is partially a consequence of a falling currency as seen in the graph above correlating inflation rates with the exchange rate of the Brazilian Real. Higher interest rates will add further pressure to government finances globally given short term financing.

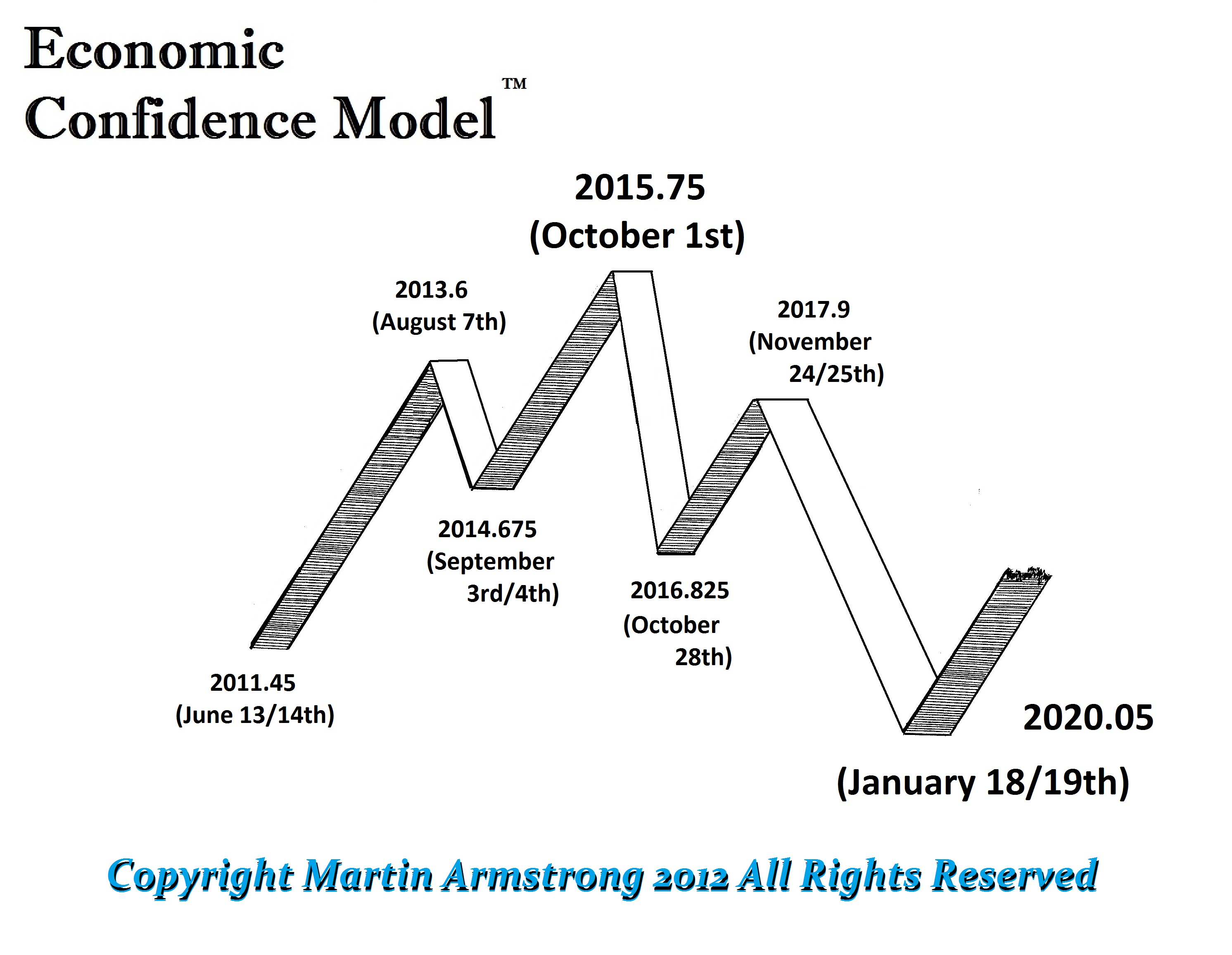

Assuming a temporary agreement is made which is looking bleak, look for Greek pressures to intensify once again in the fall along with the turn of Martin Armstrong’s Economic Confidence Model on October 1, 2015.

So why remain so confident of an eventual Greek default? With no fiscal union, the currency union is merely a currency peg. ALL currency pegs break under their own weight. While Greek polls suggest the Greeks want to remain in the EU, a large percentage of the population either works for the government or receives a government pension which are being supported by support from the Troika. According to the Brookings Institute, roughly one million people were either employed by the Greek Government or were pensioners of the public sector in 2013 as compare to a total working population of 3.8 million total workers; this is unsustainable. The Brookings institute reports that “The pension of a 55-year-old retired senior police officer is around 1,650 euros per month. A lecturer working in a university is earning around 1,200 euros (net, after tax and social security contributions).” Has anyone else noticed the absence of youth in the Greek protests? A Grexit will be painful as the government will be forced to shrink due to the lack of capital. Meanwhile, increased visibility and attractive prices will create an opportunity for entrepreneurs bringing investment capital to Greece.

Weak economic growth is fueling civil unrest globally while austerity in Europe is causing increased discontent with the EMU throughout Europe. One of the frontrunners for France’s Presidential elections, Marine Le Pen is appealing to the anti-Euro movement calling for a Frexit if the EU does not return “monetary, legislative, territorial and budget sovereignty.” When the Greek economy recovers following a Grexit, anti-Euro sentiment will only increase.

Most developed countries would be envious of 2.9% GDP growth in today’s environment, Iceland is doing just that with 1Q 2015 GDP growth of 2.9% supported by consumption and investment up 6.4% and domestic demand up 10%. Recall Iceland allowed its banks to default. In addition, Iceland only spends 9.1% of GDP on healthcare whereas the US spend 17.9% according to the CIA World Factbook of August 2014.

Markets are expected to remain volatile through the summer leading to the ECM of October 1, 2015 so pay attention to the arrays and reversals. This week of June 29th has been a target on the arrays for months in Greece, Euro, and bond markets. However, the first week of July has been a target in the Greek share market and curiously we have the referendum suddenly called for July 5th. A Grexit will cause investors to question the viability of other periphery countries such as Portugal, Spain and Italy thus pushing capital to the US. While a rally in the Euro through the summer is possible, economic weakness and political issues in Europe will continue to fuel a further rally in the USD hurting countries and corporates with USD denominated liabilities. While the bond markets may benefit from a risk-off scenario, now is the time to study corporate balance sheets and understand their exposure to higher interest rates and currency movements. All this uncertainty and volatility should cause one to pull back waiting for some clarity this next week. We remain bearish in the metals and the Chinese indices.

EU Banning Selfies Under Copyright of Architect?

Remembrance Photos in front of the Reichstag or other famous buildings in Europe could in future be banned. The European Parliament will vote on the abolition of the so-called panorama freedom. Thus a Facebook publication of vacation pictures with buildings in the background would be allowed only with the permission of the architect.

So under their insane proposed law I would need approval of Michelangelo to take this picture as I did in Rome at Christmas. This law is going down with Utah’s law which prohibits you from ordering a drink before ordering dinner.

This is why we should eliminate career politicians. They have to keep busy so they create stupid laws out of boredom.

Here Comes Puerto Rico Monday – Next Greece

Puerto Rico is set to release a key report on its financial stability Monday, and its Governor, Gov. Alejandro Garcia Padilla told The New York Times that the island would probably seek significant concessions from as many as all of its creditors because “the debt is not payable.”

Puerto Rico is the next Greece where the “vulture” investors bought their bonds back in 2013 when its roughly $70 billion in outstanding debt suffered a huge plunge in bond prices over the summer.

All government follow the same model and this is BIG BANG, where government debt at every level will begin a death spiral. Governments since World War II have borrowed continuously never managing anything properly. They have just assumed that the great herd of taxpayers had deep pockets that were endless. This attitude is causing the collapse in Socialism whereas all the promises of pensions cannot be maintained. The majority of people assumed that working for government was the safest. They are now starting to see that it is the worst of all for you cannot even prosecute them for mismanagement and fraud as you would if a private employer pulled the same nonsense.

The smart money smells a rat. Capital has rushing out of long bonds since May and pouring into the very short-term federal paper pushing rates back negative to the crisis level of 2009. BIG BANG is being furthered by the worst collapse in liquidity I have ever witnessed in my entire career.

Greece Imposes Capital Controls

Alexis Tsipras has imposed capital controls as Greek banks are to remain closed. The European Central Bank (ECB) said it was not increasing emergency funding to Greek banks, clearly trying to hurt the Greek people to force them to stay in the Euro to protect jobs in Brussels.

Greece is due to make a €1.6bn payment to the International Monetary Fund (IMF) on Tuesday – the same day that its current bailout expires. The EU refuses to understand the source of the problem is their stupidity and design of the Euro. Greece risks default and moving closer to a possible exit from the Eurozone because of the brain-dead decisions of the EU Finance ministers.

No comments:

Post a Comment