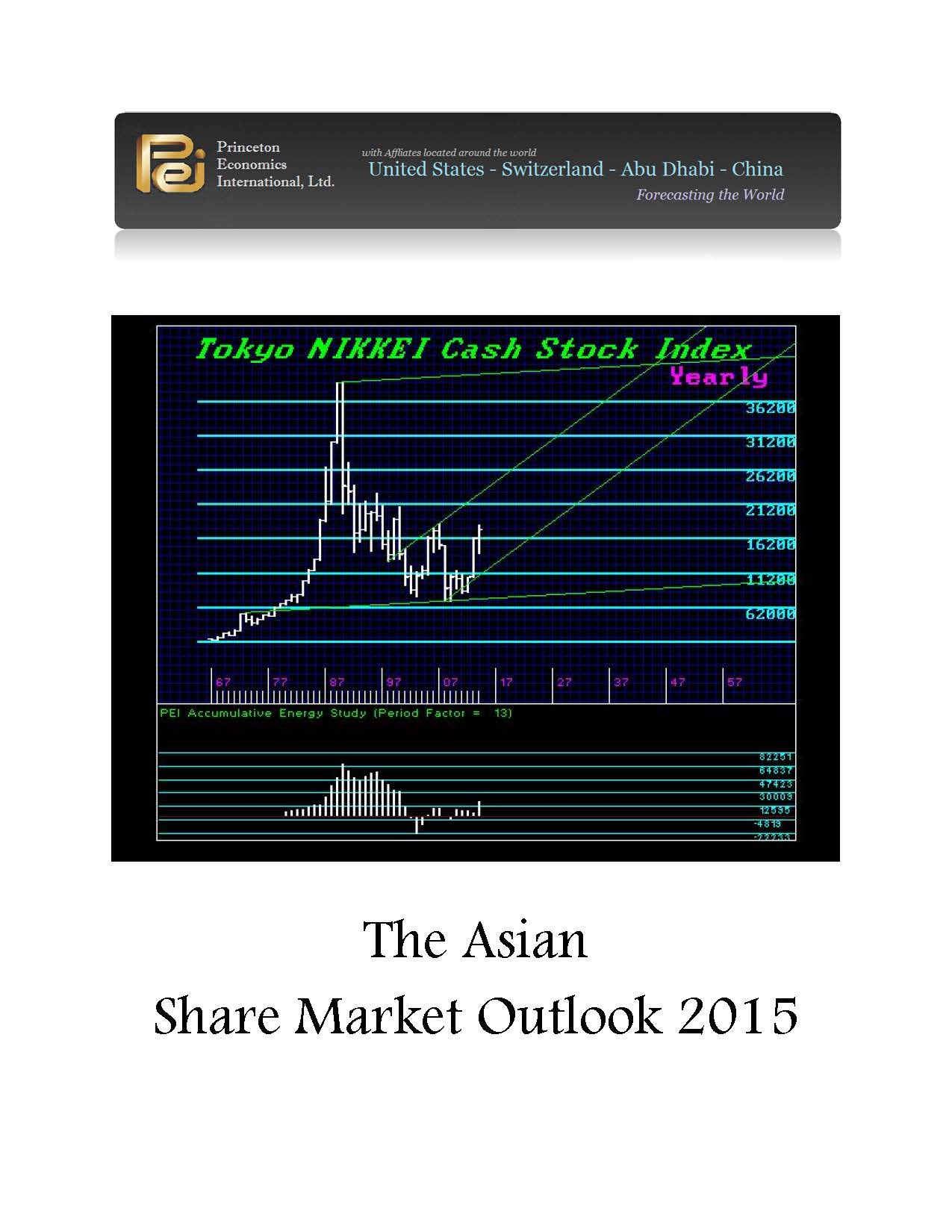

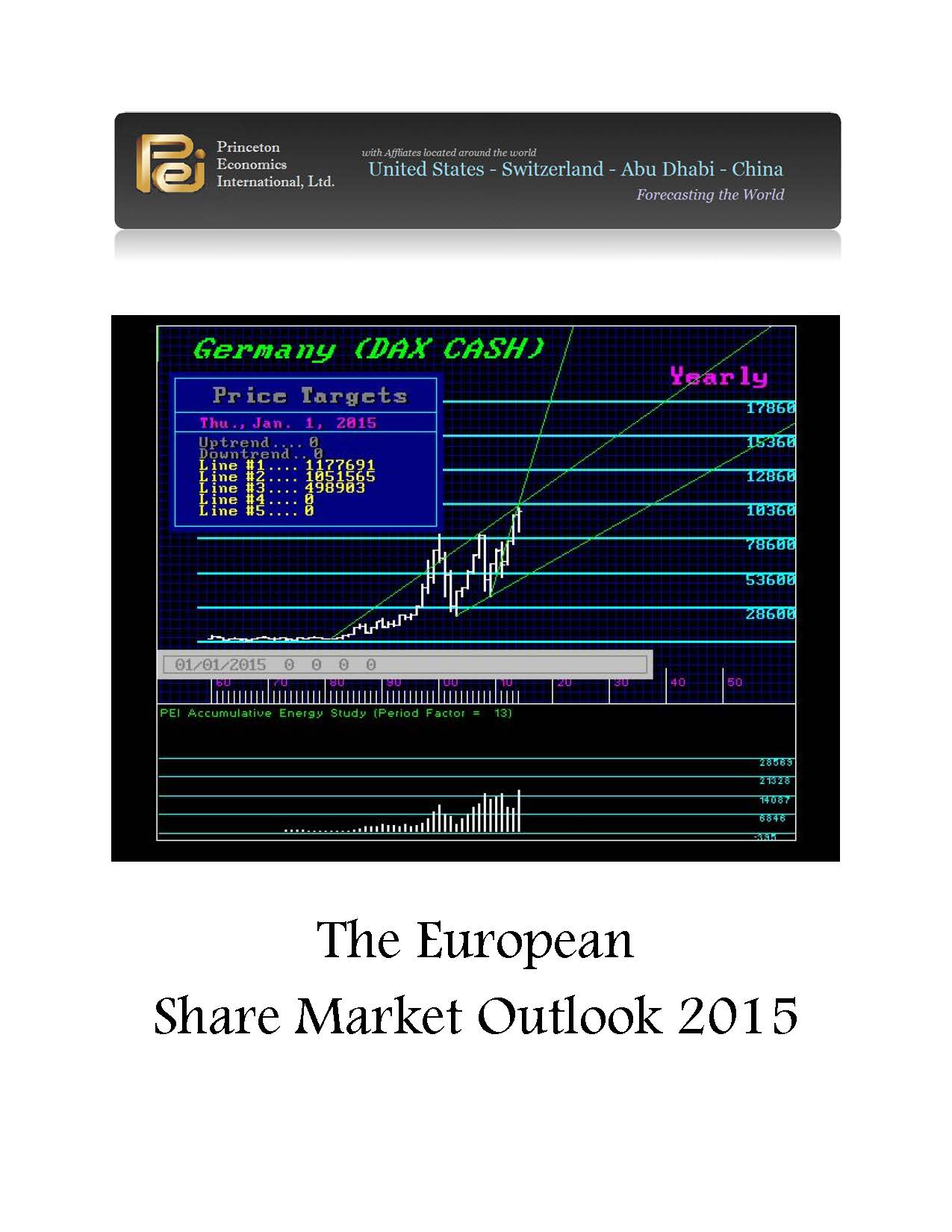

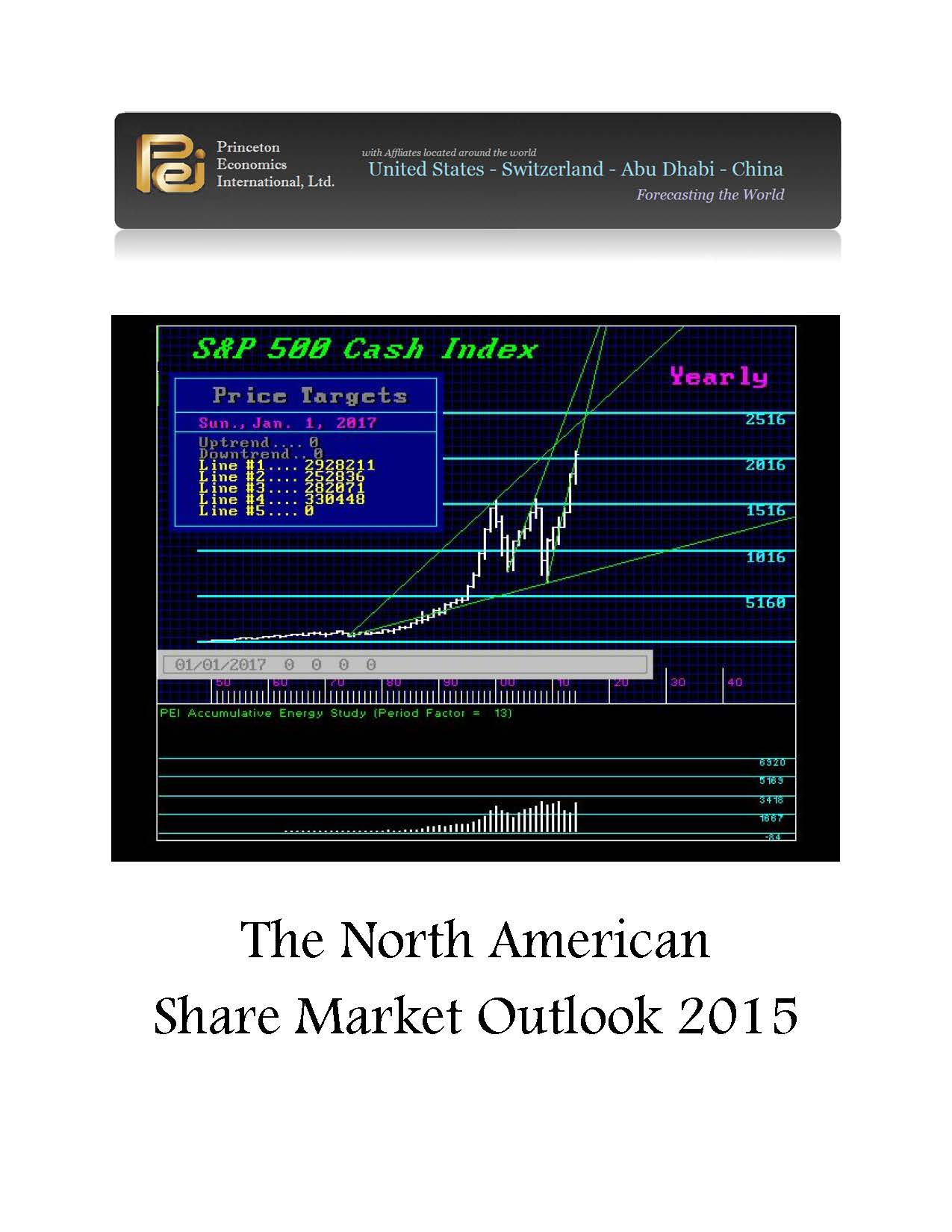

The World Share Market Reports for 2015.75

October Release of the World Share Market Reports

We are now preparing the World Share Market Reports and will not be taking orders until they are published in October. They will be available by download as well as hard copy. The set of three will be priced at US$1500. The WEC Princeton Attendees will receive the America edition and the Berlin Attendees will receiver the European edition. Those attending will be entitled to purchase the other two reports for $750.

We will also be publishing the Pension Crisis Report including interest rates, the Precious Metals Report, and an Agricultural Report. Given that this will be perhaps one of the most confusing periods to face between 2015.75 and 2017.90, we are providing historical pattern analysis so you can see what happens during such aSovereign Debt Crisis, which is becoming painfully obvious now to many.

There are always the FALSE MOVES that will cause many people to lose their shirt. This we have the high probability of watching a suspension in interest payments, widespread banking crisis, and confused governments who will respond only out of their self-interest making matters far worse as this have historically always managed to accomplish.

Gold – The Quick and Dirty

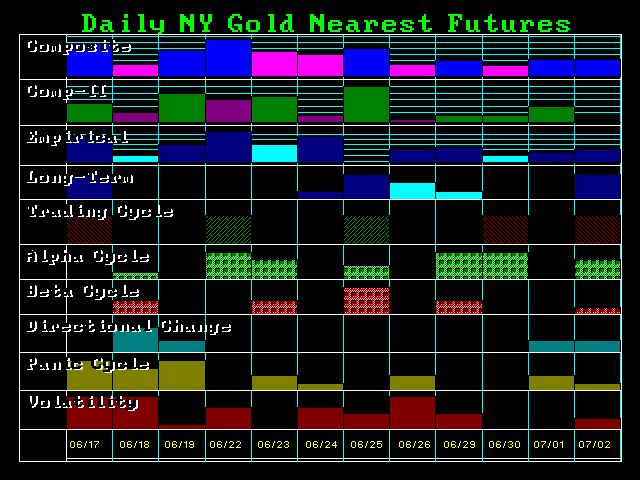

Gold has jumped back above $1200 as short positions were building up by hedge funds with no follow-through just yet. The pop is on the idea that the Fed will be raising rates slower than feared. This is the typical brain-dead analysis for anyone who bother to simply do a correlation of interest rates and inflation will quickly see that interest rates rise WITH inflation and DECLINE with DEFLATION. So it really makes no sense what they are even saying.

Nevertheless, the Directional Change hits today and the market is unfolding on time. Resistance is at 1205 and 1208 followed by 1215 and then 1225. So unless we can accomplish a daily closing above 1208 area, there is nothing to get really excited about. This is the seasonal period for a turning point in June and a high at this time will still be on schedule for the decline into at least the FIRST Benchmark target but there is a significant chance we may extend into the SECONDBenchmark Target for the final low.

Greece 2017 – Sovereign Debt Cycle

There is the old saying “Beware of Greeks bearing gifts” refers to the story of the Trojan Horse. Yet in Eastern Europe, because of the defaults of the Byzantine Empire onward, the long-standing saying was that someone was “Bankrupt like Greece.”

The two countries who are serial defaulters in Europe are France and Spain. The Spanish sovereign defaults took place, turning the country into a serial defaulter beginning in 1557 followed by 1570, 1575, 1596, 1607, and 1647 ending in a 3rd world status. Greece holds the record for the greatest duration of default by its government: it has been in default for about 50% of its modern history. Portugal also defaulted during the mid-sixteenth century. Other European states followed in the seventeenth century, including Prussia in 1683, though France and Spain remained the leading defaulters with a total of eight defaults and six defaults, respectively. Following Greek independence in 1829, Greece spent around half its time in default on its sovereign debt.

Why people even buy government debt is unexplained, for lawyers take control of government and pass laws that elevate government to “quality status” when in fact it is unsecured and has typically resulted in the total destruction of capital formation. When the core economy is involved, such as Rome, the resulting episode is typically a Dark Age.

Greece is the current deadbeat and has defaulted on its external sovereign debt obligations at least five previous times in the modern era (1826, 1843, 1860, 1894 and 1932). The first episode occurred in the early days of that country’s war of independence, and the last default was during the Great Depression in the early 1930s. The combined length under which Greece was in default during the modern era totaled 90 years, or approximately 50% of the total period that the country has been independent. This is why the Greeks tend not to pay taxes as a national sport for they also know they cannot trust government by experience.

Although many might consider this level of default to be excessive, Greece is nowhere close to the top of the list globally. Venezuela and Ecuador, with 10 defaults each in modern time, share the honor of being the greatest serial defaulters of the modern era. Yet stupidity is a virtue among bondholders for they always go back for more.

The Greek War of Independence began in 1821 with the collapse of the Ottoman Empire. The underlying dislike between Greeks and Turks extends because of this occupation. There was no “Greece” per se for the Turks ruled it for centuries. In 1824, a loan of £472,000 British pounds was secured on the London Stock Exchange to continue this fight for independence. This offering was oversubscribed and buyers were required to put down only 10% of the purchase price with a promise to pay the balance over time. An additional loan of £1.1 million pounds was floated in 1825.

Unfortunately, the London brokers kept much of the proceeds before Greece received any funds. So to a large extent, there was a real scam involved that deprived Greece of the total proceeds. Another issue was that the Greek War of Independence soon descended into civil war between rival factions, making it difficult to even determine who should receive these funds. So the brokers tended to pocket the money. Consequently, Greece technically defaulted since there was no real unified government to even make interest payments, so they were never made to the bondholders on these two loans. The bonds crashed in value and the brokers profited handsomely at the expense of the reputation of Greece. It wasn’t until 1878 that the Greek government settled on the loans, which by then with accrued interest had increased to over £10 million pounds.

In 1832, another loan totaling 60 million drachmas was given to Greece, which was officially an independent sovereign nation by that time. The loan was arranged by the French, Russian, and British governments, and was ostensibly given to help Greece build its economy and manage the initial stages of governance. However, as with most governments, corruption enters stealthily and the funds were mostly squandered on the maintenance of a military and the upkeep of Otto, a Bavarian prince who was made King of Greece by the British. Greece managed to stay current on this loan until 1843, at which time the government stopped payments. That was the same cycle when the USA went into sovereign default of the States after Andrew Jackson destroyed the central bank.

The 1843–1844 sovereign default era left a bad taste in the mouths of bondholders for once. Even the Bank of England lost money on U.S. state government debt. In the case of the 1843 Greek default, they were denied access to international credit markets for decades. During this interregnum, the government became dependent on the National Bank of Greece for borrowing. The government’s needs were modest at first, but soon escalated and the National Bank of Greece provided funds at interest rates that were twice the international lending rate.

After the Greek government was forced to settle its outstanding defaults from 1824–1825 during 1878, the global credit markets reopened once again to Greece. Greece was forced to pay off those loans that it never really received and it was a revolutionary period, not the currently established government. As always, the lenders were only too happy to provide funds once again, for they never seem to learn. This time, the new borrowing increased once again to an unsustainable level economically and the government suspended payments on external debt with the Panic of 1893. The unsound finance in the United States of the Silver Democrats led the USA into near bankruptcy in 1896 when J.P. Morgan had to lend the U.S. Treasury gold to prevent it from going bankrupt.

In 1898, foreign pressure led Greece to accept the creation of the International Committee for Greek Debt Management. This was something akin to the modern version of the IMF. This committee monitored the economic policy, tax collections, and management systems of Greece. As always, the corruption in government always results in their turning against the people to raise and enforce taxes to pay for whatever the politicians have stolen. We are approaching that same point once again in global history, not limited to Greece.

The sovereign defaults that began in 1931 in Austria set off the Great Depression that became a contagion, taking Greece down once more. Numerous countries defaulted on sovereign debt obligations from Europe, Asia, and South America, as the world economy contracted and entered what became known as the Great Depression. Even Britain suspended payments on its debt. Greece imposed a moratorium on paying on its outstanding foreign debt in 1932. This default lasted until 1964, the longest of any of the country’s five defaults. In the USA, the city of Detroit also suspended its debt payments in 1937 and finally resumed in 1963. One interesting historical anecdote is that Eleftherios Venizelos was the Greek Prime Minster that defaulted on Greece’s sovereign debt in 1932.

Evangelos Venizelos, the current Greek Deputy Prime Minister and Minister of Finance, is at the center of current crisis and heavily involved with negotiations with the European Union. The two are not related, however, and there is even unsubstantiated speculation that he changed his name to Venizelos to gain political advantage.

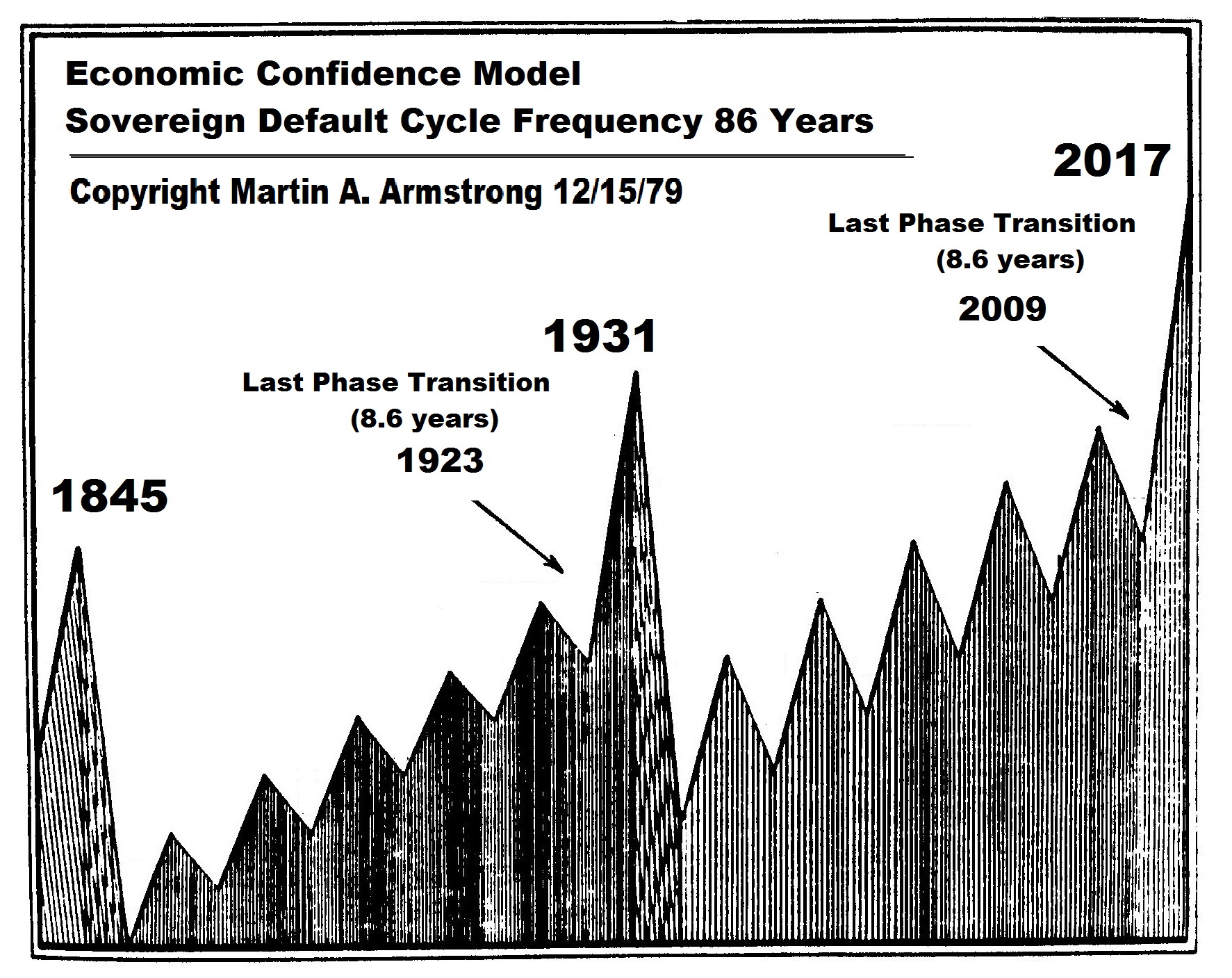

Nevertheless, we face a sovereign debt default that is not limited to Greece. The history of the financial system is not encouraging to those investors hoping that the main countries will avoid defaulting on their sovereign debt obligations. Some may take comfort in knowing that while previous defaults were dislocating to the market, the global financial system did not suffer any long-term damage because of these events, except following 1845 and 1931. These two major global defaults were interestingly 86 years apart. Adding 86 years again, curiously brings us to 2017. The whole sovereign debt crisis started to surface in 2009 which is two 86 units of time from when it began with Andrew Jackson in 1837. This is the Phase Transition on debt and we should expect the sovereign debt crisis to expand dramatically during the last phase into 2017.

Government Has Gone Insane – That’s What a Phase Transition Is All About

“Whom the gods would destroy, they first make mad,” was spoken by Prometheus in Henry Wadsworth Longfellow’s poem “The Masque of Pandora”. This seems to be very appropriate to explain our government officials for they are truly insane when it comes to economics. This is all about them sustaining a failed system that is unsupportable. They refuse to look at what they are doing and instead they are clamping down on everyone destroying the very fabric of the world economy.

I do not want to sound alarmist. However, it is critical to get the word out for when this turns down hard between 2015.75 and 2017.90, they will blame everyone but themselves. The two harbingers of economic totalitarianism, Rogoff and Buiter, are only looking at this from a purely academic perspective in a perfect world. They fail to grasp this road leads ONLY to totalitarianism, which is most likely not their intent. Nevertheless, this entire economic system is failing and all you need do is look at the collapse in liquidity in the bond markets. A trader is scared to death. Only an academic who has no such experience is oblivious to this crisis.

Meanwhile, the IMF continues to plead with the Federal Reserve not to raise rates. However, the Fed will be forced to raise rates as more capital flees to the USA with a euro meltdown. That will be heading into the only liquidity left – U.S. Equities. And there, corporates are buying back shares reducing supply.

Nevertheless, the Federal Reserve Chair, Janet Yellen, said she is encouraged by tentative signs that wage growth is picking up, but these are “not yet definitive.”This was a cautious word that the Fed is not looking at lowering rates. She said: “We have seen an increase in the growth rate of the employment-cost index, and the growth of average hourly earnings.” She continued stating: “I would call these tentative signs of stronger wage growth. I think it is not yet definitive, but that’s a hopeful sign.”

Of course, this will send the U.S. fiscal budget deficit even higher and that is more-likely-than-not going to manifest itself in a push to raise taxes. Still, we see the likelihood of a Phase Transition between 2015 and 2017 increasing dramatically. The U.S. share market continues to base at this time at higher levels. This is exceptionally positive for the broader term.

U.S. Changing Credit Card Liability on October 1, 2015

Curious note: On October 1, 2015 – the day of the Big Bang – the U.S. will begin shifting to EMV (Europay, MasterCard® and Visa®) “smart card” credit cards as a more secure way of accepting payments. Anyone accepting a card without a chip will be liable for any fraudulent payments. The banks will be exempt from accepting responsibility for fraudulent cards. Instead, the risk will shift to the merchant for accepting any non-EMV cards.

No comments:

Post a Comment